In September of 2010, I wrote a piece entitled, “Where Obama Went Wrong”. It began with this statement: “One could write an 800-page book on this subject.” Noam Scheiber has just written that book in only 368 pages. It’s called The Escape Artists and it is scheduled for release at the end of this month. The book tells the tale of a President in a struggle to create a centrist persona, with no roadmap of his own. In fact, it was Obama’s decision to follow the advice of Peter Orszag, to the exclusion of the opinions offered by Christina Romer and Larry Summers – which prolonged the unemployment crisis.

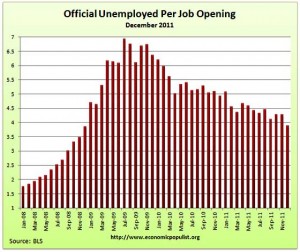

The following graph from The Economic Populist website depicts the persistence of unemployment in America:

Noam Scheiber’s new book piqued my interest because, back in July of 2009, I wrote a piece entitled “The Second Stimulus”, which began with this thought:

It’s a subject that many people are talking about, but not many politicians want to discuss. It appears as though a second economic stimulus package will be necessary to save our sinking economy and get people back to work. Because of the huge deficits already incurred in responding to the financial meltdown, along with the $787 billion price tag for the first stimulus package and because of the President’s promise to get healthcare reform enacted, there aren’t many in Congress who are willing to touch this subject right now, although some are.

The Escape Artists takes us back to the pivotal year of 2009 – Obama’s first year in the White House. Noam Scheiber provided us with a taste of his new book by way of an article published in The New Republic entitled, “Obama’s Worst Year”. Scheiber gave the reader an insider’s look at Obama’s clueless indecision at the fork in the road between deficit hawkishness vs. economic stimulus. Ultimately Obama decided to maintain the illusion of centrism by following the austerity program suggested by Peter Orszag:

BACK IN THE SUMMER of 2009, David Axelrod, the president’s top political aide, was peppering White House economist Christina Romer with questions in preparation for a talk-show appearance. With unemployment nearing 10 percent, many commentators on the left were second-guessing the size of the original stimulus, and so Axelrod asked if it had been big enough. “Abso-fucking-lutely not,” Romer responded. She said it half-jokingly, but the joke was that she would use the line on television. She was dead serious about the sentiment. Axelrod did not seem amused.

For Romer, the crusade was a lonely one. While she believed the economy needed another boost in order to recover, many in the administration were insisting on cuts. The chief proponent of this view was budget director Peter Orszag. Worried that the deficit was undermining the confidence of businessmen, Orszag lobbied to pare down the budget in August, six months ahead of the usual budget schedule. . . .

The debate was not only a question of policy. It was also about governing style – and, in a sense, about the very nature of the Obama presidency. Pitching a deficit-reduction plan would be a concession to critics on the right, who argued that the original stimulus and the health care bill amounted to liberal overreach. It would be premised on the notion that bipartisan compromise on a major issue was still possible. A play for more stimulus, on the other hand, would be a defiant action, and Obama clearly recognized this. When Romer later urged him to double-down, he groused, “The American people don’t think it worked, so I can’t do it.”

That’s a fine example of great leadership – isn’t it? “The American people don’t think it worked, so I can’t do it.” In 2009, the fierce urgency of the unemployment and economic crises demanded a leader who would not feel intimidated by the sheeple’s erroneous belief that the Economic Recovery Act had not “worked”. Obama could have educated the American people by directing their attention to a June 3, 2009 essay by Keith Hennessey (former director of the National Economic Council under President George W. Bush) which described the Recovery Act as “effective”.

Noam Scheiber’s New Republic article detailed Obama’s evolution from inexperienced negotiator to President with “newfound boldness”:

FOR TWO AND A HALF YEARS, Obama had been hatching proposals with an eye toward winning over the opposition. In most cases, all it had gotten him was more extreme demands from Republicans and not even a pretense of bipartisan support. Now, after the searing experience of the deficit deal, he still wanted reasonable, centrist policies. But he was done trying to fit them to the ever-shifting conservative zeitgeist. When he finally turned back to jobs in August, he told his aides not to “self-edit” proposals to improve their chances of passing the Republican House. “He pushed us to make sure this was not simply a predesigned legislative compromise,” one recalls.

Many readers will be surprised to learn that Larry Summers had aligned himself with Christina Romer by advocating for additional fiscal stimulus during the summer of 2009. In fact, Ms. Romer herself has already confirmed this. The Romer-Summers alliance for stimulus was also discussed in Ron Suskind’s book, Confidence Men.

As for the stimulus program itself, a new book by Mike Grabell of ProPublica entitled, Money Well Spent? provided the most even-handed analysis of what the stimulus did – and did not – accomplish. Mike Grabell gave us a glimpse of his new book with an article which appeared in The New York Times. The piece was cross-posted to the ProPublica website. Keith Hennesssey’s prescient observations about the shortcomings of that program, which he discussed in June of 2009, were somewhat consistent with those discussed by Mike Grabell, particularly on the subject of “shovel-ready” programs. Here is what Keith Hennessey said, while supporting his argument with the observations of Congressional Budget Office Director Doug Elmendorf:

In fact, the infrastructure spending in the stimulus law will peak in fiscal year 2011, which goes from October 1, 2010 to September 30, 2011. That’s too late from a macro perspective.

The Director further points out that the 2009 stimulus law created many new programs. This slows spend-out, as it takes time to create and ramp up the new programs.

The Administration has made much of working with federal and state bureaucracies to find “shovel-ready” projects to accelerate infrastructure spending. All of my conversations with budget analysts suggest this claim is tremendously overblown, and Director Elmendorf asks, “Is this practical on a large scale?”

On February 11, 2012, Mike Grabell said this:

But the stimulus ultimately failed to bring about a strong, sustainable recovery. Money was spread far and wide rather than dedicated to programs with the most bang for the buck. “Shovel-ready” projects, those that would put people to work right away, took too long to break ground. Investments in worthwhile long-term projects, on the other hand, were often rushed to meet arbitrary deadlines, and the resulting shoddy outcomes tarnished the projects’ image.

The Economic Recovery Act of 2009 will surely become a central subject of debate during the current Presidential election campaign. Regardless of what you hear from partisan bloviators, Messrs. Hennessey and Garbell have provided you with reliable guides to the unvarnished truth on this subject.