On May 22, the Congressional Budget Office released its report on how the United States can avoid going off the “fiscal cliff” on January 1, 2013. The report is entitled, “Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013”. Forget about the Mayan calendar and December 21, 2012. The real disaster is scheduled for eleven days later. The CBO provided a brief summary of the 10-page report – what you might call the Cliff Notes version. Here are some highlights:

In fact, under current law, increases in taxes and, to a lesser extent, reductions in spending will reduce the federal budget deficit dramatically between 2012 and 2013 – a development that some observers have referred to as a “fiscal cliff” – and will dampen economic growth in the short term.

* * *

Under those fiscal conditions, which will occur under current law, growth in real (inflation-adjusted) GDP in calendar year 2013 will be just 0.5 percent, CBO expects – with the economy projected to contract at an annual rate of 1.3 percent in the first half of the year and expand at an annual rate of 2.3 percent in the second half. Given the pattern of past recessions as identified by the National Bureau of Economic Research, such a contraction in output in the first half of 2013 would probably be judged to be a recession.

As the complete version of the report explained, the consequences of abruptly-imposed, draconian austerity measures while the economy is in a state of anemic growth in the wake of the 2008 financial crisis, could have a devastating impact because incomes will drop, shrinking the tax base and available revenue – the life blood of the United States government:

The weakening of the economy that will result from that fiscal restraint will lower taxable incomes and, therefore, revenues, and it will increase spending in some categories – for unemployment insurance, for instance.

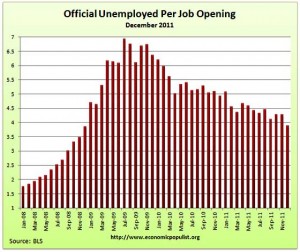

An interesting analysis of the CBO report was provided by Robert Oak of the Economic Populist website. He began with a description of the cliff itself:

What the CBO is referring to is the fiscal cliff. Remember when the budget crisis happened, resulting in the United States losing it’s AAA credit rating? Then, Congress and this administration just punted, didn’t compromise, or better yet, base recommendations on actual economic theory, and allowed automatic spending cuts of $1.2 trillion across the board, to take place instead. These budget cuts will be dramatic and happen in 2012 and 2013.

Spending cuts, especially sudden ones, actually weaken economic growth. This is why austerity has caused a disaster in Europe. Draconian cuts have pushed their economies into not just recessions, but depressions.

The conclusion reached by Robert Oak was particularly insightful:

This report should infuriate Republicans, who earlier wanted to silence the CBO because they were telling the GOP their policies would hurt the economy in so many words. But maybe not. Unfortunately the CBO is not breaking down tax cuts, when there is ample evidence tax cuts for rich individuals do nothing for economic growth. Bottom line though, the CBO is right on in their forecast, draconian government spending cuts will cause an anemic economy to contract.

Although the CBO did offer a good solution for avoiding a drive off the fiscal cliff, it remains difficult to imagine how our dysfunctional government could ever implement these measures:

Or, if policymakers wanted to minimize the short-run costs of narrowing the deficit very quickly while also minimizing the longer-run costs of allowing large deficits to persist, they could enact a combination of policies: changes in taxes and spending that would widen the deficit in 2013 relative to what would occur under current law but that would reduce deficits later in the decade relative to what would occur if current policies were extended for a prolonged period.

The foregoing passage was obviously part of what Robert Oak had in mind when he mentioned that the CBO report would “infuriate Republicans”. Any plans to “widen the deficit” would be subject to the same righteous indignation as an abortion festival or a national holiday for gay weddings. Nevertheless, Mitt Romney accidentally acknowledged the validity of the logic underlying the CBO’s concern. Bill Black had some fun with Romney’s admission by writing a fantastic essay on the subject:

Romney has periodic breakdowns when asked questions about the economy because he sometimes forgets the need to lie. He forgets that he is supposed to treat austerity as the epitome of economic wisdom. When he responds quickly to questions about austerity he slips into default mode and speaks the truth – adopting austerity during the recovery from a Great Recession would (as in Europe) throw the nation back into recession or depression. The latest example is his May 23, 2012 interview with Mark Halperin in Time magazine.

“Halperin: Why not in the first year, if you’re elected — why not in 2013, go all the way and propose the kind of budget with spending restraints, that you’d like to see after four years in office? Why not do it more quickly?

Romney: Well because, if you take a trillion dollars for instance, out of the first year of the federal budget, that would shrink GDP over 5%. That is by definition throwing us into recession or depression. So I’m not going to do that, of course.”

Romney explains that austerity, during the recovery from a Great Recession, would cause catastrophic damage to our nation. The problem, of course, is that the Republican congressional leadership is committed to imposing austerity on the nation and Speaker Boehner has just threatened that Republicans will block the renewal of the debt ceiling in order to extort Democrats to agree to austerity – severe cuts to social programs. Romney knows this could “throw us into recession or depression” and says he would never follow such a policy.

* * *

Later in the interview, Romney claims that federal budgetary deficits are “immoral.” But he has just explained that using austerity for the purported purpose of ending a deficit would cause a recession or depression. A recession or depression would make the deficit far larger. That means that Romney should be denouncing austerity as “immoral” (as well as suicidal) because it will not simply increase the deficit (which he claims to find “immoral” because of its impact on children) but also dramatically increase unemployment, poverty, child poverty and hunger, and harm their education by causing more teachers to lose their jobs and more school programs to be cut.

Mitt Romney is beginning to sound as though he has his own inner Biden, who spontaneously speaks out in an unrestrained manner, sending party officials into “damage control” mode.

This could turn out to be an interesting Presidential campaign, after all.